Blog

The latest federal budget law – officially nicknamed the One Big Beautiful Bill Act (OBBA) – is poised to cut federal Medicaid spending by nearly $1 trillion over the next decade, which could mean roughly 17 million fewer Americans on Medicaid. This blog covers the One Big Beautiful Bill Act passed and what it means for providers and clients — including the One Big Beautiful Bill Act Effective Date for major program changes.

That’s a seismic shift for a program that covers 23% of the U.S. population, including a huge share of home care clients. Home care Medicaid clients are particularly vulnerable to these changes, which is why agencies need to pay attention now.

If you’re a home care agency owner, changes to Medicaid aren’t just bureaucratic news – they hit home (quite literally) for your business.

So let’s break down OBBA’s Medicaid changes. We’ll explore what’s changing with Medicaid coverage, the new reporting and value-based payment rules (especially for managed care), and what it all means for your agency’s Medicaid compliance and bottom line. We’ll also highlight the Medicaid changes in the new bill that impact managed care and provider payments.

Let’s get into OBBA’s Medicaid changes.

One of OBBA’s most controversial moves is adding “work reporting requirements” for certain Medicaid recipients – basically a work requirement by another name. This tracks with broader pressure at the state level: Medicaid work requirement changes proposed in several states make this an even more pressing issue locally.

Starting in 2027, many adults over the age of 64 years will have to document 80 hours per month of work or community service to keep Medicaid. There’s a laundry list of exemptions (pregnant women, people with disabilities, caregivers, etc.), but the bottom line is that a lot of low-income adults could lose coverage if they can’t meet the new rules or navigate the paperwork.

Key takeaway for agencies

With tighter Medicaid eligibility and more frequent redeterminations, many “able-bodied” clients—often working irregular jobs or caregiving—could lose coverage simply for missing paperwork. That makes real-time client status tracking just as crucial as care planning.

Tools with automated monitoring and alerts—built into compliance dashboards—give agencies the visibility to catch coverage lapses early and act before care is disrupted.

And it’s not just work rules – OBBA also orders states to check eligibility more often. Remember annual Medicaid renewals? Now it’s every 6 months for expansion populations.

In other words, folks on Medicaid (especially under ACA expansion) will face twice-yearly income and status verifications. If you think Medicaid paperwork was a pain before, imagine doing it twice as often.

States can even try quarterly checks if they want. This “churn” is expected to knock off many enrollees who fail to complete a form on time. From a home care agency perspective, you might see sudden gaps in clients’ coverage. One month your client is covered, next month they’re inexplicably inactive – not because they got wealthy overnight, but because they missed a renewal notice.

Keeping track of clients’ Medicaid status is about to become as critical as the care plans you write. Agencies may find themselves reminding and assisting clients with renewal paperwork to avoid interruption in care.

Beyond individual eligibility, OBBA squeezes Medicaid at the state funding level. It limits how states can finance their share of Medicaid – notably phasing down provider taxes and capping certain payments that states use to draw federal funds.

In plain speak, states are losing some of their favorite tools to fund Medicaid. The law also ends the temporary 5% FMAP bump for expansion states (bye-bye extra federal money).

All told, states will be grappling with tighter Medicaid budgets. History shows when states feel a budget pinch, they often turn to managed care organizations (MCOs) to contain costs. And guess what MCOs do? They negotiate harder with providers, they trim reimbursement growth, and they look for efficiency.

As a home care agency, prepare for an even tougher dance with MCO contracts. States may also scale back optional services or delay rate increases. We might not feel this immediately, but in a year or two you could see rate pressure if you serve Medicaid clients, especially in states heavily hit by these funding changes (rural states and big expansion states are cited as most affected).

In short, expect Medicaid dollars to be scarcer, and plan accordingly – building a diverse payer mix or demonstrating why your services save money will be key in the OBBA era.

If there’s one buzzword you’ll be hearing even more, it’s “value-based payment”. With less money to go around, Medicaid programs are doubling down on getting more bang for each buck – i.e., paying for outcomes and quality, not just volume of services.

OBBA indirectly fuels this trend. On one hand, it puts caps on some state payments that were used to incentivize quality (like certain state-directed payments tied to hospital quality – now capped at Medicare rates).

But on the other hand, OBBA creates a $50 billion “Rural Transformation Fund” to help rural providers invest in modernizing care delivery, “encourage transitions to value-based care” and even explore things like global budgets. The message: find innovative ways to deliver care for less, and improve outcomes, especially in underserved areas.

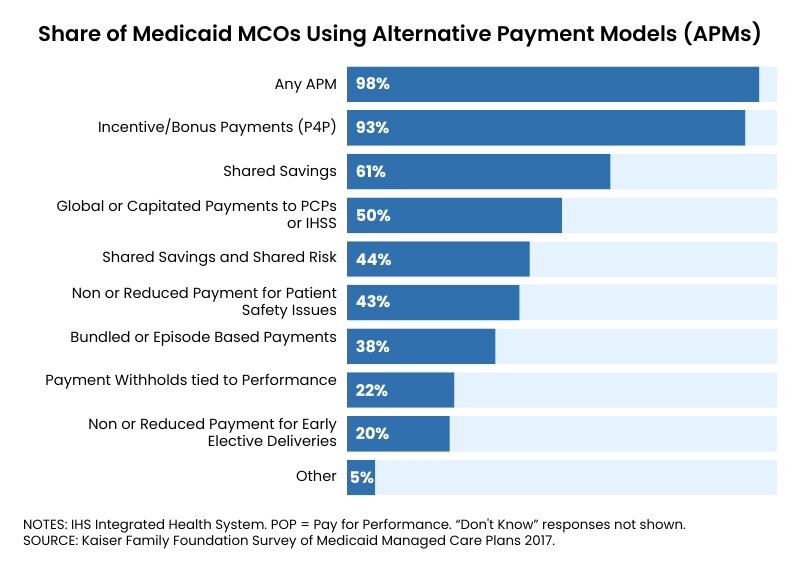

Even before OBBA, many state Medicaid programs had started requiring their MCOs to adopt value-based payment (VBP) models. Over half of states already mandate that managed care plans put a certain percentage of provider payments through alternative payment models.

Some states set specific targets or require models like accountable care arrangements, bundled payments, or shared savings. Why? To move away from the old fee-for-service (FFS) mentality. For home care agencies, this means that instead of simply being paid per visit or per hour, you may find your contracts tied to performance metrics – client satisfaction, hospitalization rates, activities achieved, etc. It might start as small bonus incentives and grow into full-blown risk-sharing down the road.

A recent survey found that nearly all Medicaid managed care plans employ at least one value-based payment arrangement to pay providers. The most universal approach is pay-for-performance bonuses tied to quality metrics (used by 93% of plans), whereas more advanced models like bundled episode payments or two-sided shared risk contracts are less common.

The trend is clear – traditional FFS is on the way out and pay-for-performance is becoming the norm.

Medicaid isn’t just tightening coverage – it’s tightening oversight. OBBA brings in new reporting requirements that aim to root out waste and fraud (the government wants to ensure every Medicaid dollar is legit).

OBBA mandates that states establish a system to verify individuals aren’t enrolled in Medicaid in two states at once, and as part of that, every MCO must report its enrollees’ address updates to the state monthly.

This might sound minor, but it’s a big procedural change. If you serve clients who move or split time between states, expect some headaches. There will be data matching galore, and possibly sudden disenrollments if someone’s flagged as getting Medicaid elsewhere.

For agencies, the practical tip is: keep your client demographics and contact info current, and emphasize to clients the importance of notifying Medicaid/MCO if they change address. A simple move could inadvertently drop someone from coverage if the system thinks they’re “out of state.”

It’s hard to argue against that one – nobody wants to bill for a deceased client. But it puts formal responsibility on providers (that includes agencies) to check the SSA death master file or otherwise ensure we’re not claiming funds for someone who passed.

In practical terms, make sure your processes immediately update client status upon death and notify the MCO/Medicaid. Delays could lead to accusations of fraudulent billing. It’s grim, but it’s now part of Medicaid compliance.

We may see states becoming quicker to recoup payments from providers for any billing errors or ineligible services. As an agency, you want to bulletproof your billing and documentation so that you’re not caught in audits with undocumented services.

The era of “slip it in and hope nobody notices” (if that ever was a thing) is over – everything must be by the book because states will be looking to retrieve misspent funds.

Let’s not forget the MCOs themselves are under the microscope. With OBBA’s changes, MCOs will have to juggle sicker pools of patients (since many healthier folks lose coverage) and less excess funding.

States will demand more reporting on outcomes and proper spending of Medicaid dollars. If you’re contracted with an MCO, be prepared for tighter reporting requirements passed down to you.

This could mean more frequent requests for patient status updates, service verification (hello, EVV – which is already mandatory nationwide for personal care), and quality data submission.

MCOs might require agencies to submit certain metrics quarterly to help the plan meet its state contract obligations.

Key takeaway for agencies

Keep demographics and client status up to date, document carefully, and automate where possible.

Platforms that integrate real-time EVV, status tracking, and billing reconciliation help minimize compliance risk—and keep audits at bay.

All these changes can make your head spin. But as a home care agency owner or manager, you can navigate this with a proactive game plan:

Value-based payment means marketing your quality as much as your quantity.

It’s okay to ask questions or seek legal/consulting help to understand new contract terms.

Don’t hesitate to share that with state Medicaid officials or legislators through industry groups.

Finally, remember that compliance isn’t just a burden – it can be a competitive advantage. Agencies that adapt quickly to OBBA’s requirements can position themselves as preferred partners for MCOs and referral sources.

It’s like being the student who always turns in homework early – you get noticed (in a good way). Yes, it’s more work. Yes, it can feel like “big brother” watching. But the heart of these changes (at least the value-based bits) is encouraging better care for the dollars spent.

Below is a handy cheat sheet summarizing major OBBA Medicaid changes and how they impact home care agencies:

| OBBA Change | What It Means for Home Care Agencies |

|---|---|

|

Work Requirements (2027) Able-bodied adults 19–64 must report 80 hrs/mo work or other qualifying activities to keep Medicaid. Many exemptions apply (pregnancy, disability, caregivers, etc.). |

Coverage Loss for Some Clients An estimated 5 million could lose Medicaid due to non-compliance. Younger adult clients may drop off rolls, reducing your client base. Agencies should prepare for interruptions in care and help connect clients with info on exemptions or alternatives. |

|

Biannual Eligibility Redeterminations Medicaid expansion enrollees must renew eligibility every 6 months instead of annually (states can opt for even more frequent checks). |

More Churn & Paperwork Clients are at higher risk of lapses in coverage due to missed paperwork. Agencies need to track clients’ Medicaid status actively. It may be wise to remind clients about renewal deadlines and assist in navigating the re-enrollment process to avoid unpaid services due to surprise disenrollments. |

|

Cutback in Federal Funding & Provider Taxes Federal Medicaid funding to states is reduced (ending expansion bonus FMAP, tighter budget neutrality on waivers, etc.), and provider tax safe harbors are lowered from 6% to 3.5% over time. |

Budget Pressure on Rates States facing funding gaps may slow reimbursement rate growth or cut optional services. They’ll likely lean on MCOs to control costs. Home care agencies should brace for tougher contract negotiations. Demonstrating cost-effectiveness (e.g. how your services prevent pricier hospital or nursing home care) will be crucial to justify rates. |

|

Value-Based Payment (VBP) Push With cost containment a priority, states are expanding managed care VBP requirements. Many states require MCOs to implement alternative payment models or meet VBP targets. OBBA’s rural demo fund also promotes shifts to value-based care models. |

Prove Your Quality or Lose Out Payment is increasingly tied to outcomes and quality metrics rather than volume. Agencies must invest in quality monitoring and reporting. Expect more performance-based bonuses or penalties in contracts. Agencies that can show data on reduced hospitalizations, high satisfaction, or improved client health will have an edge in the VBP landscape. |

|

MCO Reporting & Program Integrity Rules New mandates for data sharing and oversight: e.g., MCOs must report enrollee addresses monthly to flag duplicate state enrollment. States (and providers) must check for deceased enrollees quarterly. Overpayments are to be recouped via future payment reductions. |

More Compliance Hoops Agencies should keep client information (addresses, vital status) updated with payers to prevent inadvertent coverage termination or claim denials. Prepare for possible audits – ensure no billing for services after date of death, etc. Tighten internal compliance to avoid billing errors; mistakes will be more likely to trigger payback requests. Also be ready for MCOs asking for more frequent service data reports as they comply with new oversight regs. |

|

New Cost-Sharing for Expansion Adults (Starting 2028) Medicaid expansion enrollees >100% FPL will owe cost-sharing up to $35 per service (capped at 5% of income). Some services exempt (primary care, behavioral health, etc.), but personal care may not be exempt. |

Possible Co-pays in Home Care If your state implements this, some clients might have co-pays for home care visits. This could strain clients financially and add admin for agencies (to collect co-pays). Watch your state’s plans – if co-pays arrive, be ready to educate clients and adjust billing processes. Unpaid co-pays might become another collection issue for agencies to manage. |

Medicaid is a lifeline for millions of seniors and people with disabilities who rely on home care. Navigating these new rules is part of making sure that lifeline stays intact for them – and that your agency can continue to serve the community sustainably.

OBBA’s Medicaid changes are reshaping the playing field for home care agencies. It’s not just one policy tweak; it’s an across-the-board shift in how Medicaid defines who gets coverage, how care is paid for, and how we all account for the taxpayer’s dollar.

In some ways, it’s “back to basics” – ensuring only eligible folks are covered and demanding accountability. In other ways, it’s revolutionary – pushing healthcare toward outcomes-driven models that we’ve talked about for years but are now truly taking hold.

For a home care agency owner, the best approach is to stay informed, stay flexible, and stay client-focused. Compliance matters, but compassion and quality matter just as much. If you invest energy in both, your agency can not only survive these changes but thrive in delivering the kind of care that convinces payers (and families) that home care is the best value for money.

Download Blog